Production Concepts and the Theory of Cost

Production Concepts

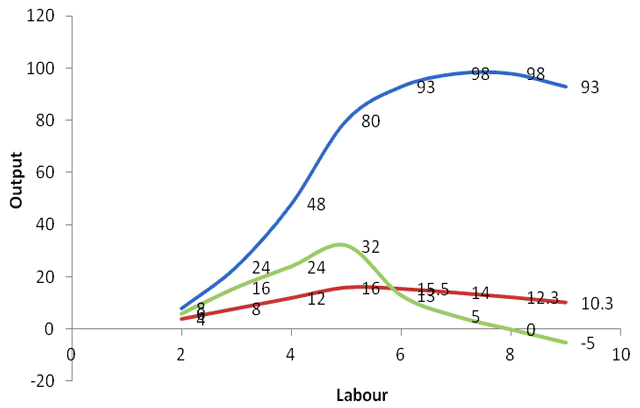

i. Total Product (TP) Total Product is the total quantity of commodities produced by a combination of factors of production at a point in time. TP is expressed as the product of Average Product and Labour units, that is: TP = AP × L

ii. Average Product (AP) AP is defined as the output per unit of the variable factor (Labour or Capital) employed. It can be obtained by dividing total product by the number of labour or capital (variable factor) employed. That is, AP \(= \frac{\text{Total Product(TP)}}{\text {Labour or Capital}}\)

iii. Marginal Product (MP) MP is the addition to total product as a result of employing an extra or additional unit of variable factor. It can be expressed as:

MP \(= \frac{\text{Change in Total Product(TP)}}{\text {Change in Variable Factor}}\)

Total, Average and Marginal Product can be presented in a table as below:

The relationship between Total Product, Average Product and Marginal Product can be represented in a graph as shown below:

EVALUATION

1.

- NEW: Download the entire term's content in MS Word document format (1-year plan only)

- The complete lesson note and evaluation questions for this topic

- The complete lessons for the subject and class (First Term, Second Term & Third Term)

- Media-rich, interactive and gamified content

- End-of-lesson objective questions with detailed explanations to force mastery of content

- Simulated termly preparatory examination questions

- Discussion boards on all lessons and subjects

- Guaranteed learning